If you’ve been reading about investing in India as an NRI, you’ve almost certainly come across three letters: SIP.

A Systematic Investment Plan is the single most practical way for NRIs to start building wealth in India, and there’s a reason it keeps coming up in every conversation we have with clients. It’s simple, it’s automated, and it’s designed for people who don’t want to think about the Indian stock market every day.

But “simple” doesn’t mean there’s nothing to understand. How a SIP actually works, why it suits NRIs specifically, what it means for your taxes, and how to avoid the common mistakes, that’s what this guide covers. If you haven’t confirmed your eligibility yet, start with “can NRIs invest in mutual funds“.

What a SIP Actually Is (And Why It Suits NRIs Perfectly)

A SIP is an automated way to invest a fixed amount into a mutual fund at regular intervals, typically monthly. Instead of investing a large lump sum all at once (and worrying about whether you’re buying at the right time), you invest small, consistent amounts every month. The fund house automatically debits the amount from your linked NRE or NRO account on a date you choose.

Each month, your SIP amount buys units of the mutual fund at that day’s price (called the NAV, Net Asset Value). When the market is down, your fixed amount buys more units. When the market is up, it buys fewer. Over time, this averages out your purchase cost, a concept called rupee cost averaging, and removes the pressure of trying to time the market.

Here’s why this matters so much for NRIs specifically:

You’re in a different time zone. You’re not watching the Indian market during trading hours. A SIP doesn’t need you to. It runs automatically on the date you set, whether you’re in a meeting in London or asleep in San Francisco.

You’re busy with life abroad. SIPs require zero intervention after setup. No monthly decisions, no manual transfers, no logging into anything. Your wealth builds in the background while you focus on your career, family, and life.

Consistency beats timing. The data on this is unambiguous. Investors who stay consistent with SIPs over 7–10 years have historically never lost money in the Nifty 50, regardless of when they started. NRIs who try to time entry points from abroad almost always end up waiting indefinitely.

You can start very small. Most SIPs allow you to begin with ₹500 per month, roughly USD 6. There’s no barrier to entry. You can scale up over time as your confidence and income grow.

How Much Should You Invest in a SIP?

This is one of the first questions NRIs ask us, and there’s no universal number, but there is a practical framework.

Start with what you can comfortably commit to every month for at least 3–5 years without needing to stop. That’s the real benchmark. A SIP that runs consistently for 10 years at ₹10,000/month will outperform a ₹50,000/month SIP that gets paused after 18 months because “something came up.”

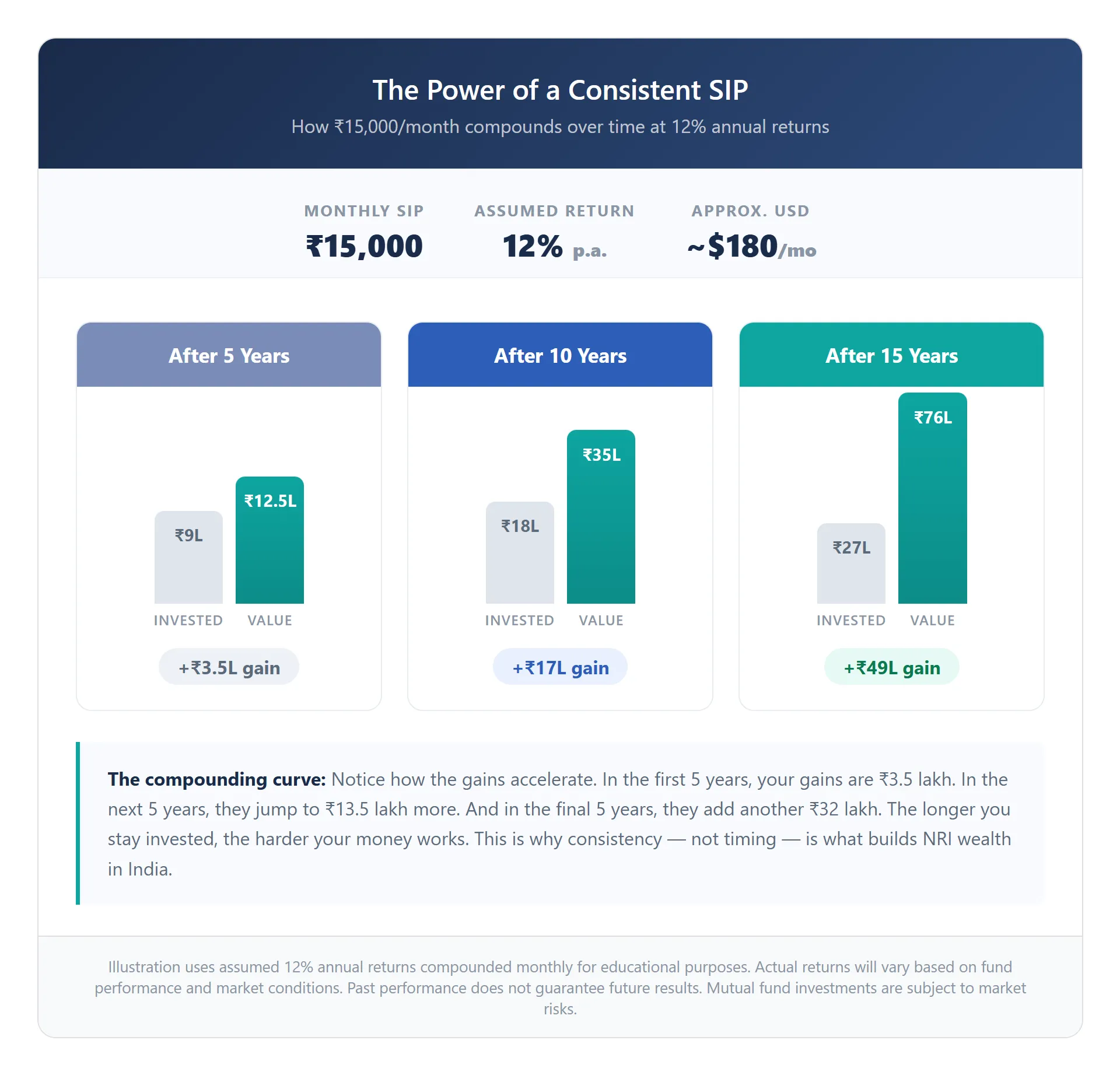

To give you a sense of scale: a ₹15,000/month SIP (roughly USD 180) invested in a fund delivering 12% annual returns over 15 years would grow to approximately ₹75–76 lakh, from a total investment of ₹27 lakh. The compounding does the heavy lifting, but only if you stay in long enough to let it work.

Step-up SIPs are something we often recommend to NRIs. Instead of keeping your SIP amount the same every year, you increase it by 10–15% annually, ideally when your salary goes up. A ₹10,000 SIP stepped up by 10% yearly grows your corpus dramatically compared to a flat SIP over the same period. Most fund houses support this feature, and we can set it up for you.

The specific amount and fund selection depends on your goals, your risk comfort, and your timeline. That’s a conversation we’re happy to have, it’s one of the things we do best.

SIP Through NRE or NRO, Which Account Should You Use?

This is an important choice that many NRIs don’t think about until it causes a problem. “NRE vs NRO account“

SIP through NRE account: Your investment is classified as repatriable. When you eventually redeem your mutual fund units, the proceeds can be sent back abroad freely. This is the right route for most NRIs investing money earned overseas.

SIP through NRO account: Your investment is classified as non-repatriable (or subject to the USD 1 million per year repatriation cap). This route is for money that originated in India, rental income, pension, inheritance. It works fine for investing, but moving the proceeds abroad later involves additional compliance.

The mandate matters. For a SIP to debit automatically each month, you need a standing instruction (mandate) linked to your NRE or NRO account. Setting this up correctly, with the right bank, the right mandate type, and properly linked to the fund house, is where many NRIs face failed transactions or delayed start dates.

We set up SIP mandates for NRIs routinely, and we make sure the bank linkage, mandate registration, and fund house onboarding all work together from day one. If you’d rather not troubleshoot failed debits on your own, let us handle it.

The Tax Nuance Every NRI Must Understand About SIPs

Most NRIs know the broad tax rates for mutual funds: 12.5% on long-term equity gains (over 12 months) and 20% on short-term gains (under 12 months). “NRI mutual fund taxation“

But here’s the part that catches people off guard: each SIP installment is treated as a separate purchase with its own 12-month holding period.

So if you’ve been running a SIP for 14 months and you redeem your entire holding, only your first 2 months of units qualify as long-term (taxed at 12.5%). The remaining 12 months of units are still short-term (taxed at 20%).

This is why we always advise NRIs: don’t redeem your entire SIP holding in one go unless you genuinely need all of it. Redeem strategically, oldest units first, and let as much of your portfolio cross the 12-month mark as possible. This alone can save you a meaningful amount in tax.

TDS (Tax Deducted at Source) is automatically deducted by the fund house whenever you redeem, so you’ll see the tax impact immediately. If too much TDS is deducted (which happens when the fund house applies the higher rate on all units), you can claim a refund by filing an Indian income tax return.

Tax structuring around SIPs is one of the areas where we add significant value. The right redemption strategy can make a real difference to your after-tax returns.

Common SIP Mistakes NRIs Make

Stopping the SIP during market dips. This is the single most damaging mistake. Market dips are exactly when your SIP buys more units at lower prices, that’s the entire point of rupee cost averaging. NRIs who pause SIPs during corrections and restart during rallies end up buying high and missing the recovery. Stay the course.

Not stepping up. Running the same SIP amount for 10 years means you’re investing a shrinking proportion of your income over time. Step up by at least 10% annually.

Picking funds based on last year’s returns. Top-performer lists change every year. A fund that ranked #1 last year might rank #30 this year. Fund selection should be based on consistency, fund manager track record, and how the fund fits within your overall portfolio, not a single year’s performance.

Not linking the mandate correctly. A SIP that fails to debit for 3 consecutive months gets automatically cancelled by most fund houses. This usually happens because the bank mandate wasn’t set up properly or the NRE/NRO account didn’t have sufficient balance on the debit date. We’ve seen this catch many NRIs off guard.

Redeeming too early. A SIP needs time to compound. The real wealth creation happens in years 7–15, not years 1–3. If you’re pulling money out after 2 years, a SIP wasn’t the right vehicle for that goal, a fixed deposit would have been.

Frequently Asked Questions

Let Us Get Your SIP Running

The SIP itself is simple once everything behind it is set up correctly, the account, the KYC, the mandate, the fund selection. Getting all of that aligned from abroad, without delays or failed debits, is where our team makes a real difference. “how to get set up from abroad“

We’ve set up SIPs for NRIs across 30+ countries. We handle the end-to-end process, account alignment, mandate registration, fund selection based on your goals, and ongoing support if anything needs adjusting.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. The SIP growth illustration uses assumed returns of 12% p.a. for illustrative purposes only, actual returns may vary and are subject to market risks. Tax laws and FEMA regulations are subject to change. Mutual fund investments are subject to market risks, please read all scheme-related documents carefully.